2025 Year-End Tax Tips and Strategies for Business Owners

2025 Year-End Tax Tips for Business Owners

As 2025 comes to a close, many business owners are thinking about wrapping up their books, reviewing results, and getting ready for a new year. But before December 31 passes, there’s one more important task to tackle — your year-end tax strategy.

A few smart moves now can reduce your tax bill, protect your company’s cash flow, and create new planning opportunities for 2026. Here’s how to make the most of the weeks ahead.

Strengthen Year-End Cash Flow

Strong cash flow is the foundation of good tax planning. Before year-end, take time to review how much cash your business needs to meet short-term obligations such as payroll, supplier invoices, or loan payments.

If your taxable income is higher than expected, look for ways to reduce or defer taxes by:

-

Accelerating deductible expenses (for example, professional fees, utilities, or rent).

-

Writing off bad debts or setting up reserves for doubtful accounts.

-

Paying out reasonable bonuses or salaries before year-end, if already declared.

You may also want to delay income into 2026 by deferring invoices or delaying the sale of appreciated assets, depending on your overall income picture.

Managing cash flow now can free up funds to reinvest in your business — or take advantage of new deductions and credits before they expire.

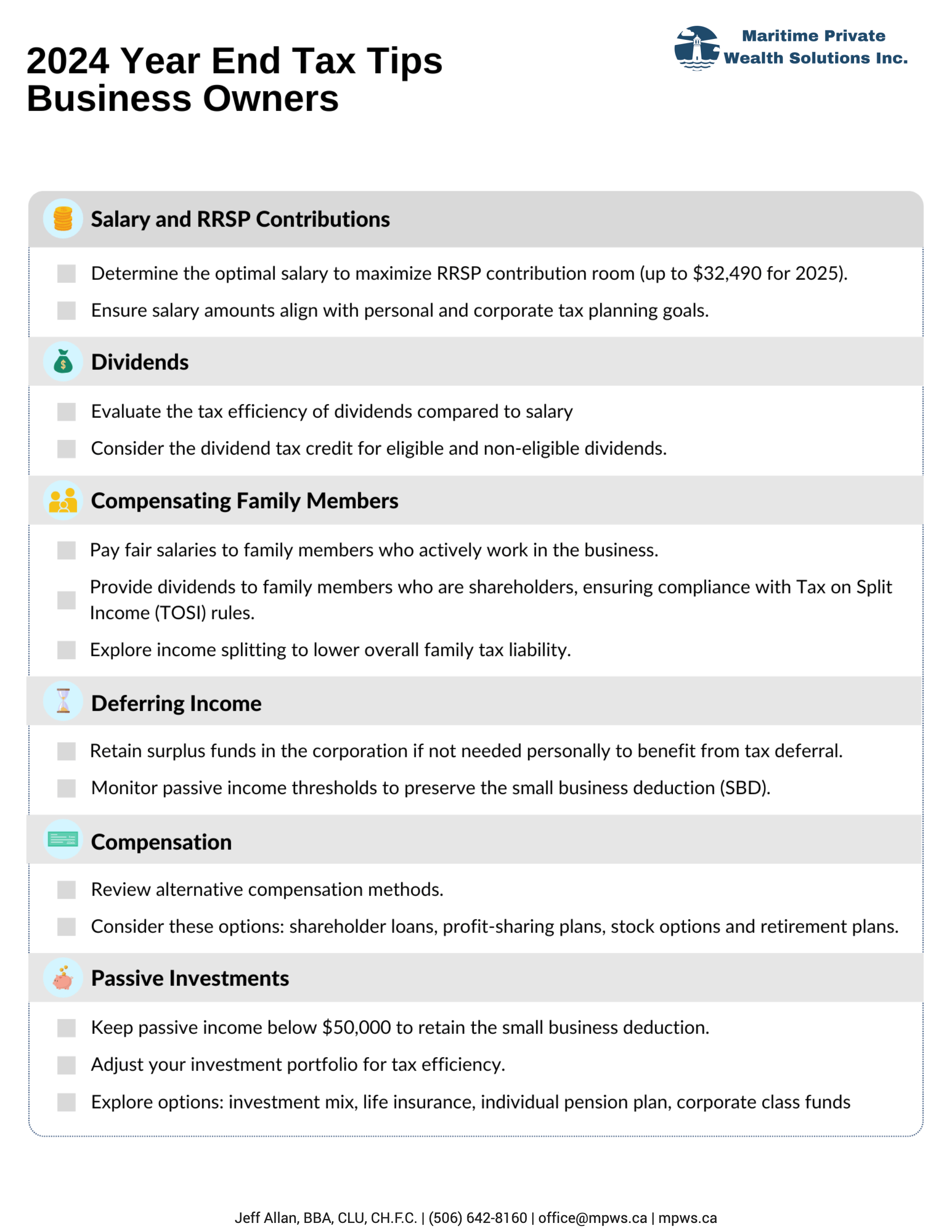

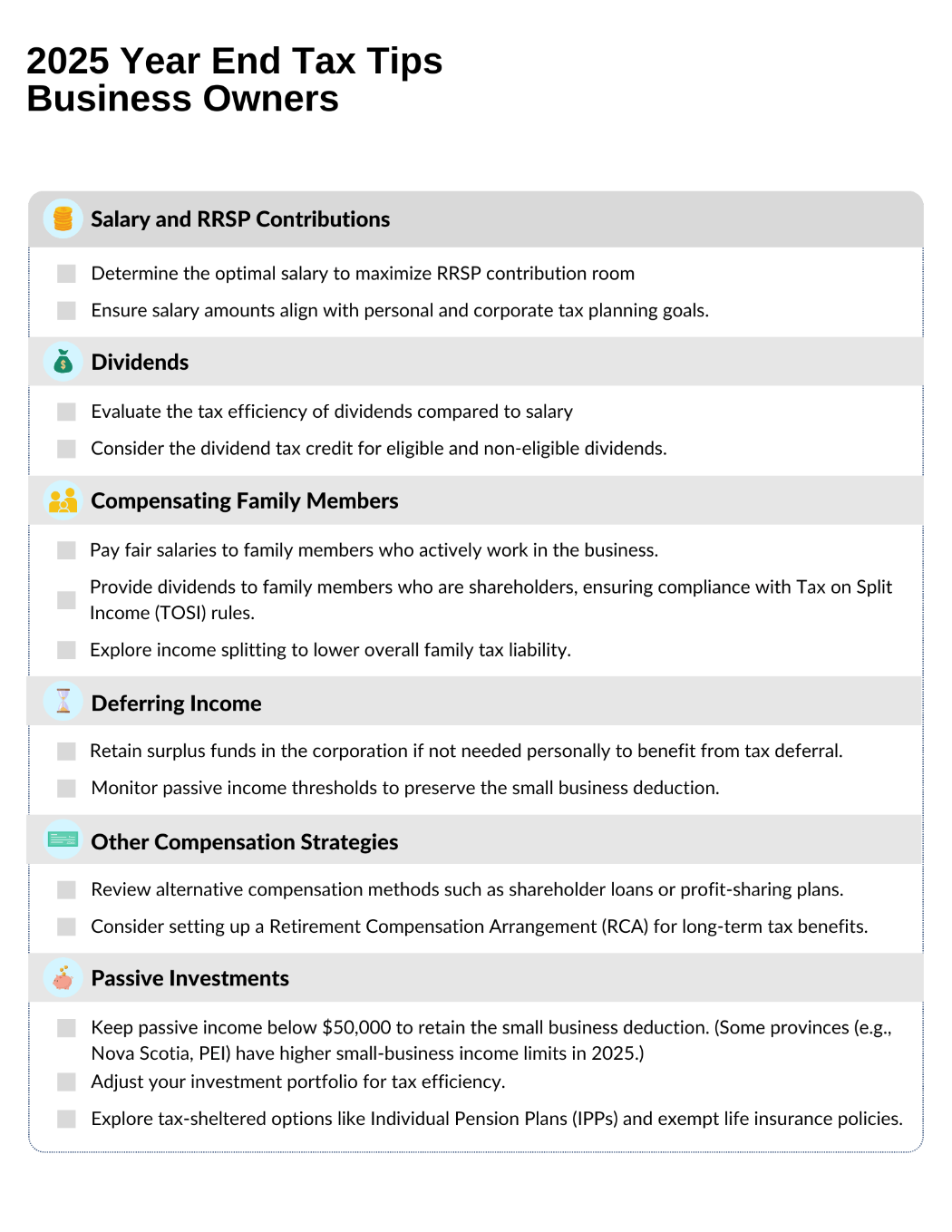

Optimize Your Salary and Dividend Mix

For incorporated business owners, one of the most important year-end decisions is how to pay yourself.

Salary provides earned income that creates RRSP contribution room and qualifies for Canada Pension Plan (CPP) benefits. Dividends, by contrast, are taxed at a lower rate in most provinces and don’t require CPP contributions.

For 2025, earning $180,500 in 2024 creates the maximum RRSP room of $32,490 for 2025. Looking ahead, for 2026 contributions, $187,833 in 2025 salary will be needed to reach the increased RRSP limit of $33,810. If you mainly use dividends, make sure you earn enough salary to keep building RRSP room. The RRSP deadline for 2025 is March 2, 2026.

A balanced mix often provides the best outcome — salary for savings and CPP, and dividends for flexibility. Review your compensation with your accountant before the year ends to lock in your approach.

Family Income and Compensation Planning

If family members are involved in your business, paying them can be a practical and tax-efficient option:

-

Salaries to Family Members: Paying a fair salary to family members who work for your business not only compensates them but also gives them access to RRSP contributions and CPP. You must be able to prove the family members have provided services in line with the amount of compensation you give them.

-

Dividends to Family Members: If family members are shareholders, dividends can provide them with tax-efficient income. The tax-free amount varies by province or territory, so it’s worth checking the rules where you live.

-

Income Splitting: Distributing income among family members can help reduce overall taxes. However, be mindful of the Tax on Split Income (TOSI) rules to avoid penalties. A tax professional can guide you through this process.

Deferring Income

If you don’t need the full amount for personal use, leaving surplus funds in the corporation could be a smart move. This keeps the money invested within the business, benefiting from lower corporate tax rates. Over time, this approach may allow the funds to generate more income compared to personal investing, depending on your goals and investment strategy. However, be mindful of passive investment income limits, as exceeding $50,000 in passive income could reduce or eliminate your corporation’s access to the small business deduction. Monitoring this threshold is essential to maintaining the tax advantages available to your business.

Other Compensation Strategies

It’s always a good idea to review how you handle compensation beyond base salary.

Consider these options:

-

Shareholder Loans: Borrow funds from your corporation with deductible interest but ensure repayment to avoid personal tax.

-

Profit-Sharing Plans: These can be a tax-efficient alternative to bonuses for distributing profits.

-

Stock Options: Only the employee or employer—not both—can claim a deduction when options are cashed out.

-

Retirement Plans: Explore setting up a Retirement Compensation Arrangement (RCA) to save for retirement tax-efficiently.

Passive Investments

Canadian-controlled private corporations (CCPCs) benefit from a reduced corporate tax rate on the first $500,000 of active business income, thanks to the small business deduction (SBD). The SBD can lower the tax rate by 12% to 21%, depending on your province or territory. Some provinces (e.g., NS, PEI) changed small-business limits in 2025, which may affect combined rates.

However, passive investment income over $50,000 in the previous year reduces the SBD by $5 for every additional dollar, potentially eliminating it altogether. To maintain access to the SBD, it’s important to keep passive investment income below this threshold.

Here are some strategies to help preserve your SBD:

-

Defer Portfolio Sales: Delay selling investments that generate capital gains if possible.

-

Optimize Your Investment Mix: Focus on tax-efficient investments like equities over fixed income.

-

Exempt Life Insurance Policies: Income earned within these policies isn’t included in your passive investment total.

-

Individual Pension Plan: This defined benefit plan is exempt from passive income rules and offers tax-advantaged retirement savings.

Carefully managing passive investments can help your business maintain access to the SBD and maximize its tax advantages for continued growth.

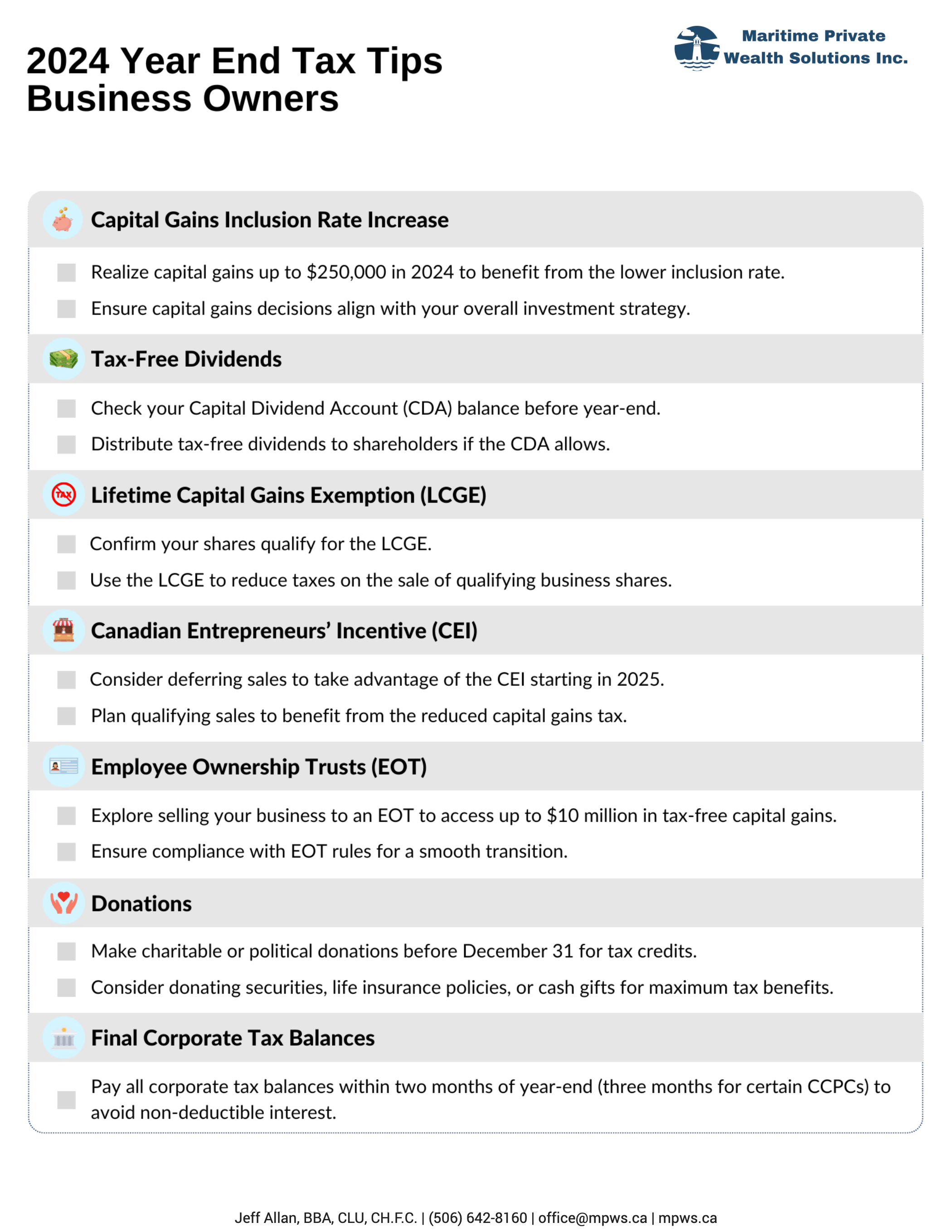

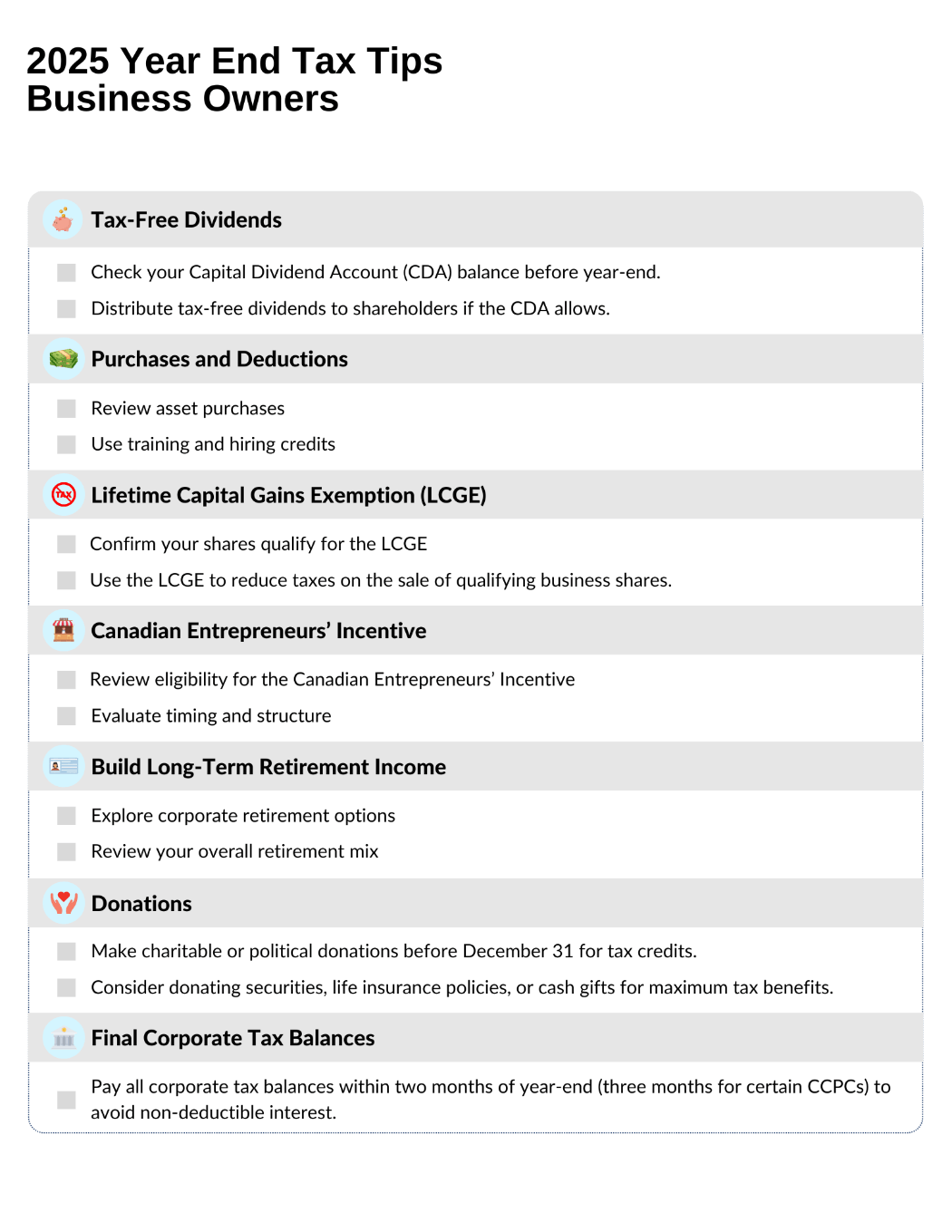

Use Your Capital Dividend Account (CDA) Wisely

The Capital Dividend Account lets private corporations pay tax-free dividends from specific sources, such as the non-taxable portion of capital gains or certain life insurance proceeds.

If your CDA has a positive balance, it may be worth paying out a capital dividend before realizing any capital losses, which can reduce the CDA balance. Once losses are recorded, your ability to pay tax-free dividends is reduced or eliminated.

A quick check with your advisor before year-end can ensure you don’t miss this opportunity.

Take Advantage of Purchases and Deductions

If you’re planning to buy equipment or technology for your business, timing your purchases before December 31 can offer valuable deductions.

Under current tax measures, certain business assets qualify for enhanced depreciation or immediate expensing. Select assets can qualify for a 100% first-year write-off under Budget 2025 proposals for property available for use before 2030. This measure allows businesses to accelerate deductions and reduce taxable income in the year the asset is placed in service.

Making these investments now may lower your 2025 taxable income while positioning your business for growth.

Apprenticeship and Training Incentives

Many provinces offer refundable credits for hiring and training apprentices in skilled trades. These credits vary by region but can offset a meaningful portion of training costs.

Taking advantage of these incentives supports your workforce, rewards innovation, and improves your bottom line.

Plan for Business Transition and Succession

If you’re thinking about selling or passing down your business in the future, 2025 brings several important planning opportunities.

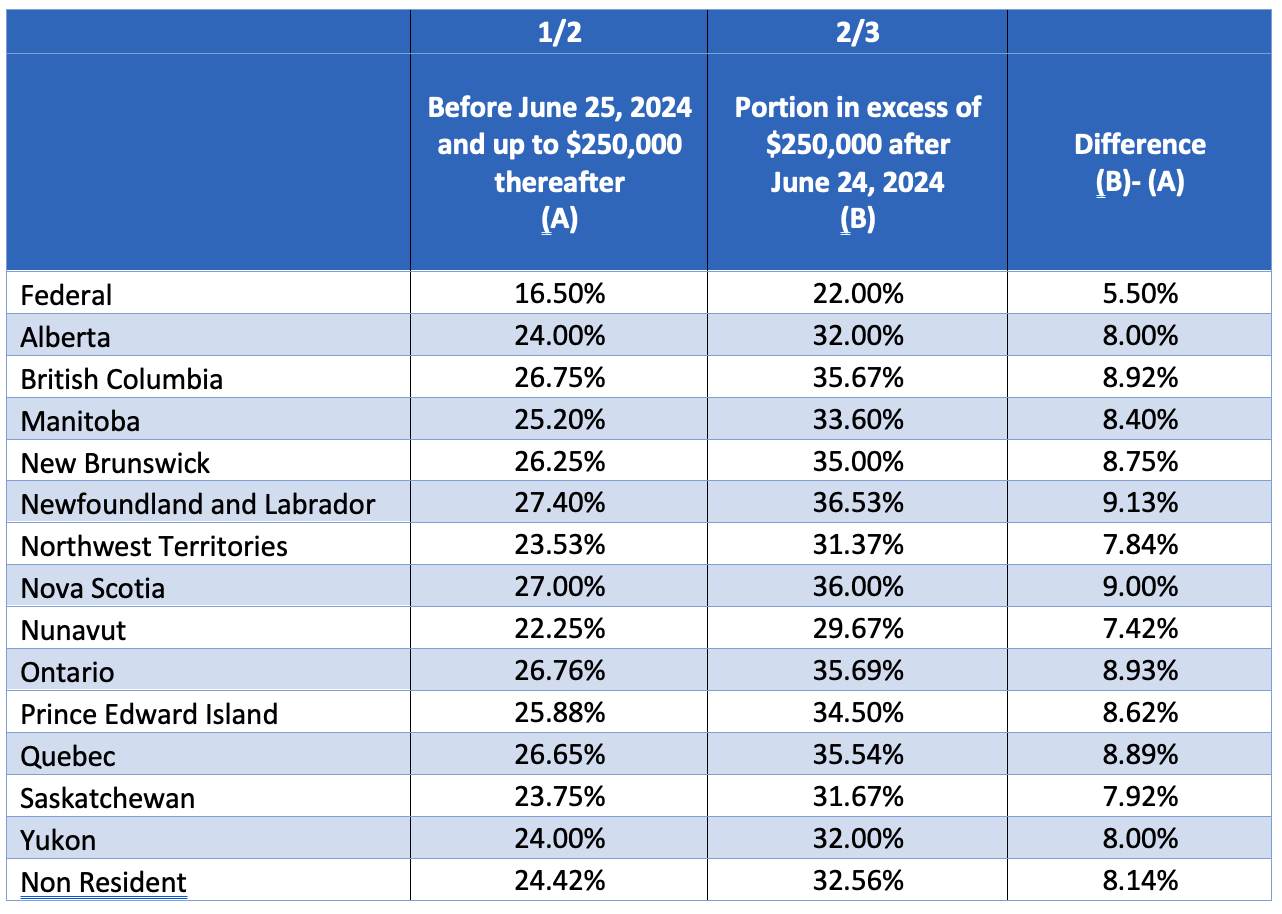

The Lifetime Capital Gains Exemption (LCGE) lets you shelter up to $1.25 million (indexed after 2025) in capital gains from tax when selling qualified small business corporation (QSBC) shares.

Starting this year, the new Canadian Entrepreneurs’ Incentive (CEI) further reduces tax on eligible business sales by lowering the capital gains inclusion rate to one-third on up to $2 million of gains over your lifetime. This new incentive phases in gradually over five years.

If your shares qualify for these exemptions, you may wish to crystallize (lock in) the exemption now or review your ownership structure to ensure you meet all conditions. Proper planning can make the difference between a fully taxable gain and one that’s largely tax-free.

Build Long-Term Retirement Income

While many owners reinvest profits into their business, it’s important to plan for your own financial future as well.

Here are a few corporate-friendly retirement options to consider:

-

Individual Pension Plans allow for higher contribution limits than RRSPs, particularly for owners over age 40 with consistent income.

-

Retirement Compensation Arrangements let you set aside corporate funds for future retirement on a pre-tax basis.

-

Employee Profit Sharing Plans can be used to share profits with employees in a tax-efficient way.

Reviewing your long-term savings approach ensures that the wealth you build in your company also supports your personal retirement goals.

Donations

Making donations, whether charitable or political, can provide valuable tax benefits. To maximize these advantages, consider options like:

-

Donating securities

-

Giving a direct cash gift to a registered charity

-

Using a donor-advised fund for ongoing charitable contributions

-

Setting up a private foundation

-

Donating a life insurance policy by naming a charity as the beneficiary or transferring ownership.

Each option offers unique tax advantages depending on your situation.

Bringing It All Together

Year-end planning isn’t just about saving on taxes — it’s about making intentional financial decisions that support your business’s next chapter.

By reviewing your compensation, investments, and future goals before December 31, you can lower taxes today while setting the stage for long-term success.

Consider scheduling a meeting with your accountant or advisor soon to discuss which of these strategies fit your business best. A small amount of preparation now can make a big difference in 2026.

Sources:

CPA Canada, “2024 Federal Budget Highlights,” https://www.cpacanada.ca/-/media/site/operational/sc-strategic-communications/docs/02085-sc_2024-federal-budget-highlights_en_final.pdf?rev=6d565a6a66ef4e20b1e01dc784464c93, 2024.

Government of Canada, “Capital Gains Inclusion Rate,” https://www.canada.ca/en/department-finance/news/2024/06/capital-gains-inclusion-rate.html, 2024.

Advisor.ca, “Lifetime Capital Gains Exemption to Top $1M in 2024,” https://www.advisor.ca/tax/tax-news/lifetime-capital-gains-exemption-to-top-1m-in-2024/, 2024.

PwC Canada, “Year-End Tax Planner,” https://www.pwc.com/ca/en/services/tax/publications/guides-and-books/year-end-tax-planner.html, 2024.

CIBC, “2024 Year-End Tax Tips,” https://www.cibc.com/content/dam/personal_banking/advice_centre/tax-savings/year-end-tax-tips-en.pdf, 2024.

Government of Canada, “Federal Budget 2024,” https://budget.canada.ca/2024/report-rapport/tm-mf-en.html, 2024.