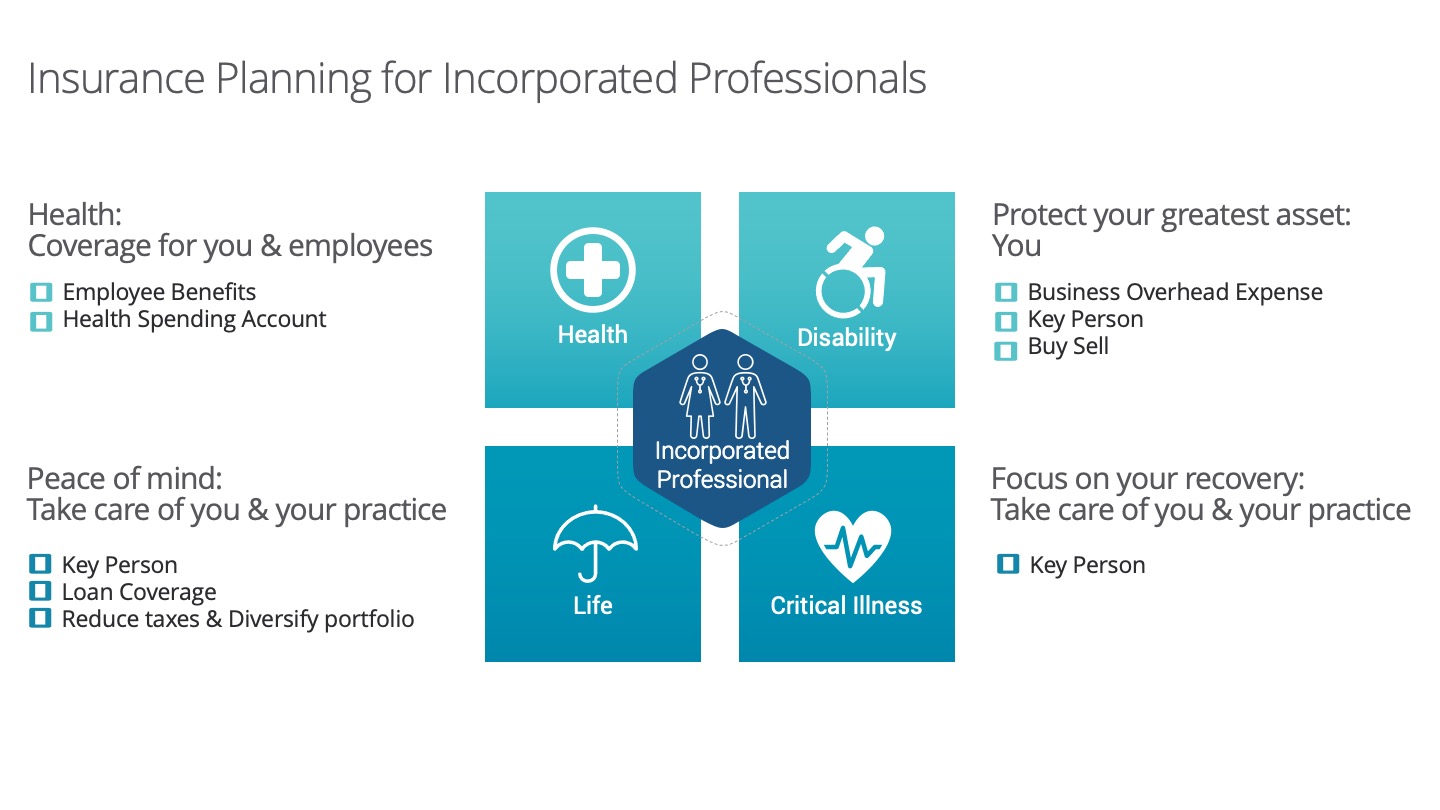

Why a Critical Illness Insurance Top-Up Could Make a Big Difference

Most of us don’t expect to face a serious illness in our lifetime. But the truth is, health challenges such as cancer, heart disease, or stroke are more common than many people realize. In fact, about half of Canadians will develop cancer at some point in their lives. The question is—would your family or business be financially ready if something unexpected happened?

Critical illness insurance is designed to provide a lump-sum payment if you’re diagnosed with a covered illness. Many employees have some level of coverage through work, and some business owners purchase policies personally. But here’s the challenge: the amount of coverage included in a standard policy often isn’t enough to fully protect your income, household, or business. That’s where a “top-up” comes in.

Adding extra coverage can help close the gap, offering peace of mind and flexibility at a time when you’d want to focus fully on recovery.

Understanding the gap in coverage

Group insurance provided through an employer is a valuable benefit, but it usually comes with limits. For example, coverage amounts may be capped at a set level, such as $25,000 or $50,000. While helpful, this amount might not go far if you’re facing months away from work or costly medical treatments not fully covered by government health care.

For families, this shortfall can mean dipping into savings or going into debt just to keep up with everyday bills. For business owners, it could mean not having enough cash flow to keep operations running smoothly while stepping away to focus on health. A top-up ensures your coverage reflects your actual financial responsibilities, not just a general amount offered in a group plan.

Why families consider a top-up

If you’re raising children or supporting loved ones, an unexpected illness can bring financial stress on top of emotional strain. Mortgage payments, daycare costs, grocery bills, and education savings don’t pause when life takes a turn. A top-up can provide additional funds to help cover household expenses or even allow a spouse to take time off work to provide care.

Think of it as a financial cushion that allows your family to focus on what matters most—supporting your recovery—without the added worry of how to make ends meet.

Why employees might need more than their work plan

Relying only on your workplace benefits can leave you underinsured. Employer coverage usually ends if you change jobs, retire, or if your company makes changes to its benefits package. That means you could lose coverage at a time when it might be harder to qualify for new insurance.

By topping up your coverage personally, you’re not only increasing your protection—you’re also making sure you have something portable that stays with you, no matter where your career takes you. This stability can be especially valuable for professionals in industries where job changes are common.

Why business owners look at top-ups differently

For business owners, the stakes are even higher. A serious illness doesn’t just affect you personally—it can affect your entire company. From paying employees and suppliers to covering rent and utilities, your business may still need to run while you’re focused on treatment and recovery.

A top-up can provide a financial buffer to keep things running smoothly. It may also give you flexibility to hire temporary help, reduce workload, or take the time you need without rushing back before you’re ready. This not only protects your own livelihood but also helps safeguard your employees and clients who depend on you.

The benefits of a top-up

When deciding whether to add more coverage, here are some of the benefits families, employees, and business owners often value:

- Peace of mind: Knowing you’re covered beyond the basics can relieve stress.

- Financial flexibility: The lump-sum payment can be used for anything—from medical costs to everyday expenses.

- Control: Unlike some insurance benefits, you choose how the funds are used.

- Portability: A personal top-up stays with you, even if your job changes.

- Business continuity: For entrepreneurs, extra coverage can help keep the business stable while you recover.

At its core, a critical illness insurance top-up is about creating a stronger safety net. It’s about having the right level of protection for your specific needs, rather than relying on a “one-size-fits-all” amount that may fall short.

Life is unpredictable, but preparing for the unexpected can make a big difference. By topping up your coverage, you’re helping ensure that if illness strikes, you and your loved ones can focus on what really matters—healing and moving forward.

If you’re unsure how much coverage is right for you, it may help to review your current benefits, your family’s expenses, and any business obligations you’re responsible for.

This is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult a qualified professional regarding your specific situation. We are not responsible for any actions taken based on this content.