Financial Checklist for New Parents in Canada

What to Do Financially When You Have a Baby

A new baby brings a lot of joy, and a lot of new to-do lists. Most of them are about feeding schedules and car seats. But a few items on the list are about money, and they matter more than you might think.

You do not need to do everything at once. A newborn keeps you busy enough. The steps below can be spread out over the first few months. Think of this as a simple checklist you can come back to as you find the time and energy.

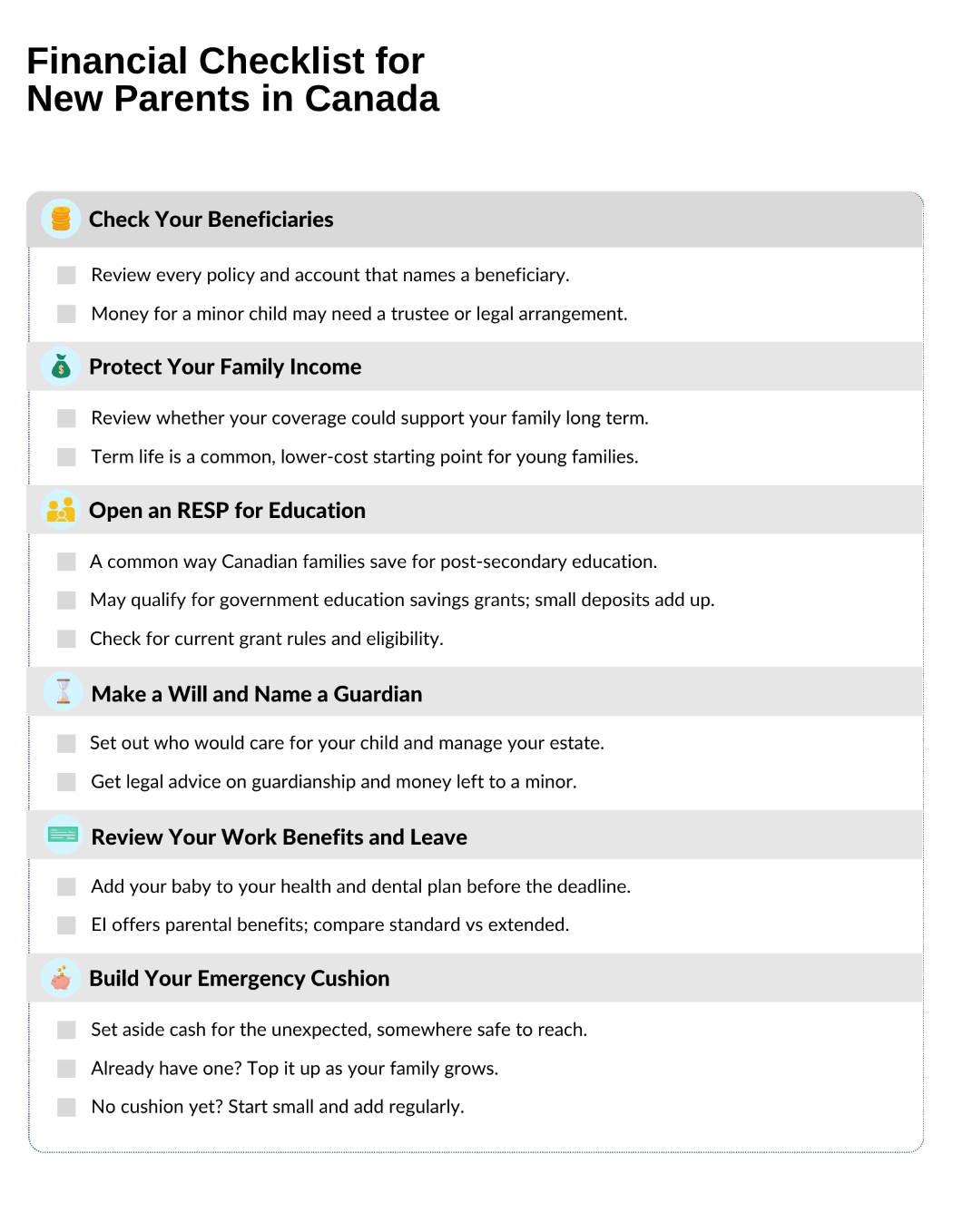

Check Your Beneficiaries

A beneficiary is the person who receives the money from your life insurance or certain registered accounts after you pass away. Many people set these up years ago and never look at them again.

Now is a good time to check. You may want to add your partner, update an older choice, or think through how money should be handled for your child. If you want money to go to a minor child, it may need to be managed through a trustee or other legal arrangement until the child is of age, depending on the asset and the province.

The key point is simple. Look at every policy and account that names a beneficiary, and make sure the names and instructions still match the life you have today.

Protect Your Family Income With Life Insurance

When it was just you, or just you and your partner, a gap in income may have been easier to manage. With a baby who depends on you, the stakes are higher. Life insurance can help protect your family financially if something happens to you, so they can keep up with housing costs, bills, and daily expenses.

For many young families, term life insurance is a common starting point. It covers you for a set number of years, often when your children are young and your financial obligations are highest. The premiums are usually lower than permanent coverage, which can make it easier to fit into a new-parent budget.

Your need for coverage often increases when you have a child. It is worth checking whether your current coverage, including any through work, would be enough to support your family for more than just the short term.

Open an RESP for Education

A Registered Education Savings Plan, or RESP, is a common way Canadian families save for a child’s post-secondary education. One reason many parents use it is the government support that can come with it through education savings grants.

You do not need a large amount to begin. Even small, regular deposits can add up over time. Check canada.ca for the current grant rules, contribution details, and eligibility requirements.

Make a Will and Name a Guardian

This is the step many new parents put off, and it is one of the most important. A will helps set out who would care for your child and how your estate should be handled if you and your partner die.

For parents, the most important part is often naming the person you want to care for your child. In BC, a will can express your wishes about guardianship, but it is also important to work with proper legal advice so your will deals clearly with both the care of your child and the management of any money left to a minor.

If you already have a will, a new baby is a good reason to review it. Add your child, confirm your choices, and make sure your estate plan still reflects your wishes.

Review Your Work Benefits and Leave

Your job may offer more help than you realize. Many group benefit plans allow you to add a new dependent, but the deadline depends on the plan. Check with your human resources team or plan administrator as soon as possible after the birth so you do not miss the deadline for health and dental coverage.

Employment Insurance, or EI, also offers maternity and parental benefits for eligible parents. Parents can choose standard or extended parental benefits, and the timing and number of weeks differ between the two options, so it is important to review the current rules before applying.

Build Your Emergency Cushion

A baby comes with surprises, and some of them cost money. An emergency cushion is simply cash set aside for the unexpected, kept somewhere safe and easy to reach.

If you already have one, this is a good time to top it up. A larger family often means larger surprise costs. If you do not have one yet, start small. Even a modest amount set aside regularly can help keep a rough week from becoming a money crisis.

A Calm Way to Start

That is a full list, and you do not have to tackle it all at once. Pick one item this week. Maybe it is checking a beneficiary, or asking work about adding your baby to your benefits. Small steps, taken one at a time, can help build a stronger financial foundation for your growing family.

This content is provided for general informational purposes only. It is not intended to provide investment, tax, or legal advice, and should not be relied upon as such.

Sources: